Beranda

/ Insurance Deductible On Rental Property : Top 6 Tax Deductions For Rental Owners East Bay Property Management And Consulting / I'm only out ~$2,300 (my policy deductible) waiting until aug to do the repair (when hail season is over) reminder to all:

Insurance Deductible On Rental Property : Top 6 Tax Deductions For Rental Owners East Bay Property Management And Consulting / I'm only out ~$2,300 (my policy deductible) waiting until aug to do the repair (when hail season is over) reminder to all:

Insurance Gas/Electricity Loans Mortgage Attorney Lawyer Donate Conference Call Degree Credit Treatment Software Classes Recovery Trading Rehab Hosting Transfer Cord Blood Claim compensation mesothelioma mesothelioma attorney Houston car accident lawyer moreno valley can you sue a doctor for wrong diagnosis doctorate in security top online doctoral programs in business educational leadership doctoral programs online car accident doctor atlanta car accident doctor atlanta accident attorney rancho Cucamonga truck accident attorney san Antonio ONLINE BUSINESS DEGREE PROGRAMS ACCREDITED online accredited psychology degree masters degree in human resources online public administration masters degree online bitcoin merchant account bitcoin merchant services compare car insurance auto insurance troy mi seo explanation digital marketing degree floridaseo company fitness showrooms stamfordct how to work more efficiently seowordpress tips meaning of seo what is an seo what does an seo do what seo stands for best seotips google seo advice seo steps, The secure cloud-based platform for smart service delivery. Safelink is used by legal, professional and financial services to protect sensitive information, accelerate business processes and increase productivity. Use Safelink to collaborate securely with clients, colleagues and external parties. Safelink has a menu of workspace types with advanced features for dispute resolution, running deals and customised client portal creation. All data is encrypted (at rest and in transit and you retain your own encryption keys. Our titan security framework ensures your data is secure and you even have the option to choose your own data location from Channel Islands, London (UK), Dublin (EU), Australia.

Insurance Deductible On Rental Property : Top 6 Tax Deductions For Rental Owners East Bay Property Management And Consulting / I'm only out ~$2,300 (my policy deductible) waiting until aug to do the repair (when hail season is over) reminder to all:. You can only deduct homeowner's insurance premiums paid on rental properties. I'm only out ~$2,300 (my policy deductible) waiting until aug to do the repair (when hail season is over) reminder to all: You can deduct the expenses paid by the tenant if they are deductible rental expenses. All of the above can be detrimental to the property and pose significant risk, both to the occupant, but also to your investment as a whole. A new roof is considered an capital improvement that increases the basis of your rental property.

I have a rental property and insurance covered replacing my roof minus the deductible. You generally treat mortgage insurance on rental property loans and mortgages as an ordinary and necessary business rental expense that you deduct on schedule e against the income from that rental property. You have the additional protection of being able to deduct the cost of damages in the event of theft, floods, earthquakes, and hurricanes. Homeowner's insurance protects you against loss from damage to the property. It gets included as a part of all rental income received.

Landlord Insurance Vs Homeowners Insurance from www.rentecdirect.com If you have employees, you can deduct the cost of their health and workers' compensation insurance too. Insurance premiums you pay on your rental property are deductible from your income tax. But property insurance is covering the repair. Depending on the type of loan, you could pay the mortgage insurance either in a lump sum or annually as you make your mortgage payments. If your rental property is completely destroyed or stolen, your deduction is calculated as follows: You must keep in mind that you can only deduct the amount for the current year, not any premiums paid in advance for the next year. In general, you can deduct mortgage insurance premiums in the year paid. So, if you run your rental property under a separate business or llc, your personal umbrella policy (attached to your home or auto insurance, for example) may not be applicable.

If you receive rental income from your home and you're a landlord:

So, if you run your rental property under a separate business or llc, your personal umbrella policy (attached to your home or auto insurance, for example) may not be applicable. This requires business liability insurance. As a landlord, you can deduct a number of expenses you incur as the owner of a rental property on your income tax return. Therefore a payout from the insurance company is reportable rental income. You generally treat mortgage insurance on rental property loans and mortgages as an ordinary and necessary business rental expense that you deduct on schedule e against the income from that rental property. Luckily, any form of insurance is considered an ordinary and necessary rental property expense and is thus deductible. Unfortunately, there is no average cost for landlord insurance. Never is homeowner's insurance tax deductible your main home. If you are a rental property owner than you can deduct certain expenses to get lower tax rates. If your rental property is completely destroyed or stolen, your deduction is calculated as follows: Umbrella insurance policies that offer extra liability insurance are also a deductible expense along with mortgage insurance and flood insurance. This includes fire insurance, theft insurance and the health and workers' insurance you pay for employees of. Most business owners share these tax perks, but the finer details can differ a bit at tax time.

In general, you can deduct mortgage insurance premiums in the year paid. You can only deduct homeowner's insurance premiums paid on rental properties. This includes mortgage insurance premiums that are paid on the rental property. Insurance premiums you pay on your rental property are deductible from your income tax. Rental property insurance protects property investors in the event of damage or loss to a dwelling while it is rented or leased to tenants.

Choosing A Renters Insurance Deductible Valuepenguin from res.cloudinary.com If you have employees, you can deduct the cost of their health and workers' compensation insurance too. If your policy gives coverage for more than one year, deduct only the premiums related to the current year. Insurance premiums you pay on your rental property are deductible from your income tax. What do i include on my property assets depreciation section? Your adjusted basis is the property's original cost, plus the value of any improvements, minus any deductions you took for regular or bonus depreciation or section 179 expensing. Rental property insurance protects property investors in the event of damage or loss to a dwelling while it is rented or leased to tenants. If your rental property is completely destroyed or stolen, your deduction is calculated as follows: The answer to the main question is—your homeowners insurance is tax deductible for your rental property.

However, if you prepay the premiums for more than one year in advance, for each year of coverage you can deduct only the part of the premium payment that will apply to that year.

Insurance premiums you pay on your rental property are deductible from your income tax. Unfortunately, there is no average cost for landlord insurance. When you own several properties and those properties are used only for rental income, then all of. Report the deduction on line 9 of schedule e (form 1040), supplemental income and loss. Most schedules e for mortgaged properties show tax losses, not profits. This is a benefit of renting a property since you cannot deduct your homeowners insurance for the property you reside in. Most business owners share these tax perks, but the finer details can differ a bit at tax time. If your policy gives coverage for more than one year, deduct only the premiums related to the current year. If you own a rental property or rent out your primary residence (or part of it) from time to time, you may be able to deduct your expenses, including homeowners insurance costs. You have the additional protection of being able to deduct the cost of damages in the event of theft, floods, earthquakes, and hurricanes. Costs will vary based on the state, county, city and even block your rental property is located on. In general, you can deduct mortgage insurance premiums in the year paid. If so, the deduction will not work for you anyway.

Luckily, any form of insurance is considered an ordinary and necessary rental property expense and is thus deductible. If so, the deduction will not work for you anyway. Lastly, you can restructure your business to allow for a clean health insurance deduction, via creating a separate property management business, but this is on the advanced side, not for a quick online tip. You have the additional protection of being able to deduct the cost of damages in the event of theft, floods, earthquakes, and hurricanes. Your adjusted basis is the property's original cost, plus the value of any improvements, minus any deductions you took for regular or bonus depreciation or section 179 expensing.

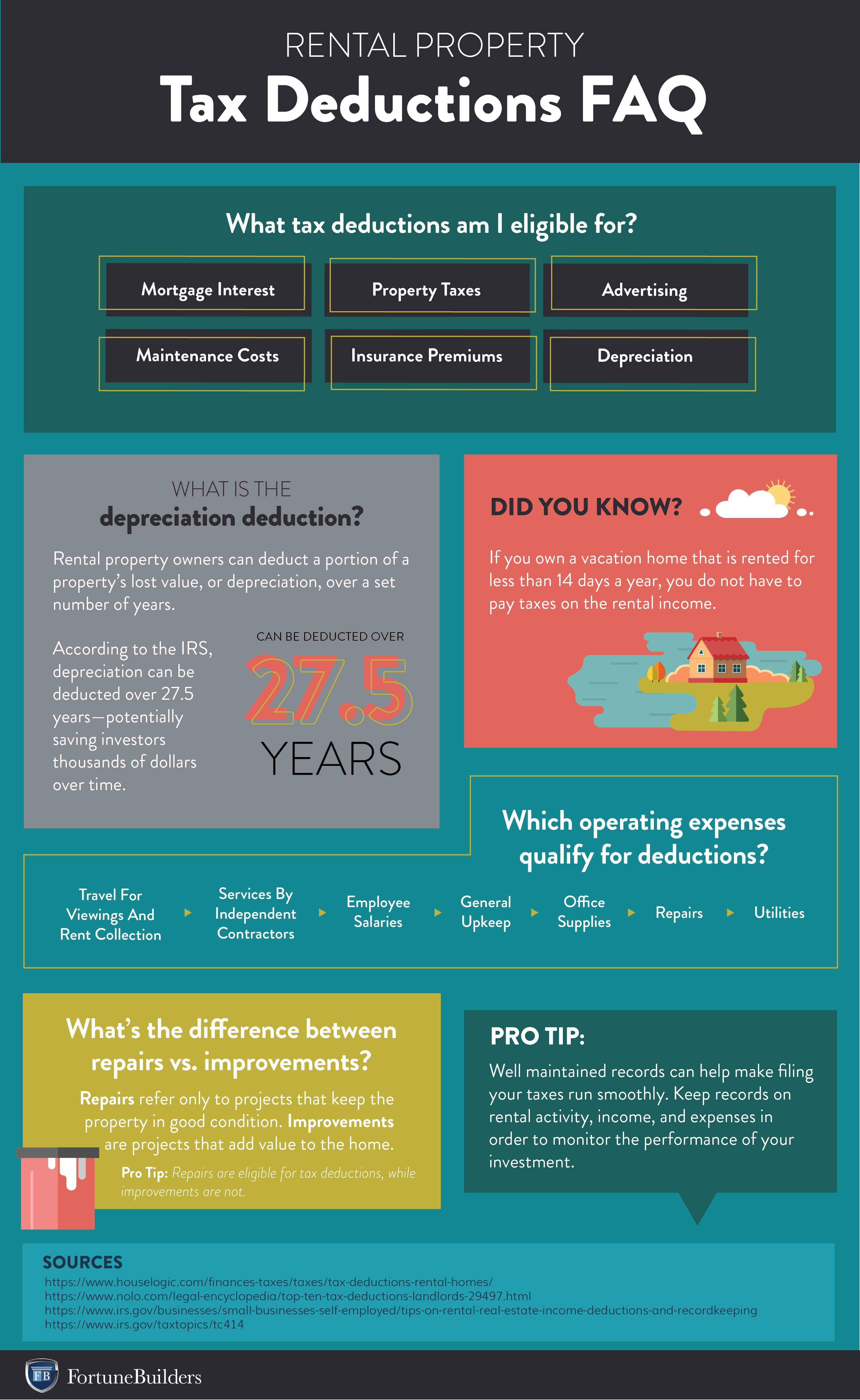

How Is Rental Income Taxed What You Need To Know Fortunebuilders from www.fortunebuilders.com So, if you run your rental property under a separate business or llc, your personal umbrella policy (attached to your home or auto insurance, for example) may not be applicable. You can only deduct homeowner's insurance premiums paid on rental properties. Deductions include mortgage interest, property taxes, depreciation on the. If you have employees, you can deduct the cost of their health and workers' compensation insurance too. Deduct the remaining premiums in the year (s) to which they relate. A rental property owner may take a deduction for casualty losses only to the extent that the loss is not covered by insurance. Others choose to hold property in an llc as a business entity. You generally treat mortgage insurance on rental property loans and mortgages as an ordinary and necessary business rental expense that you deduct on schedule e against the income from that rental property.

All of the above can be detrimental to the property and pose significant risk, both to the occupant, but also to your investment as a whole.

If you own a rental property or rent out your primary residence (or part of it) from time to time, you may be able to deduct your expenses, including homeowners insurance costs. So, if you run your rental property under a separate business or llc, your personal umbrella policy (attached to your home or auto insurance, for example) may not be applicable. Never is homeowner's insurance tax deductible your main home. Depending on the type of loan, you could pay the mortgage insurance either in a lump sum or annually as you make your mortgage payments. If your policy gives coverage for more than one year, deduct only the premiums related to the current year. You have the additional protection of being able to deduct the cost of damages in the event of theft, floods, earthquakes, and hurricanes. You can even deduct a proportional amount of. Others choose to hold property in an llc as a business entity. If you have employees, you can deduct the cost of their health and workers' compensation insurance too. If you are a rental property owner than you can deduct certain expenses to get lower tax rates. Although you might pay them both, keep in mind that mortgage insurance and homeowner's insurance aren't the same thing: I'm only out ~$2,300 (my policy deductible) waiting until aug to do the repair (when hail season is over) reminder to all: You should have rental income after direct expenses, insurance, and property taxes, and you can take a depreciation deduction to offset the taxes on that income.